economy-investment

Saudi Arabia enters Kearney FDI top 10 — climbing from 24th to 10th in three years

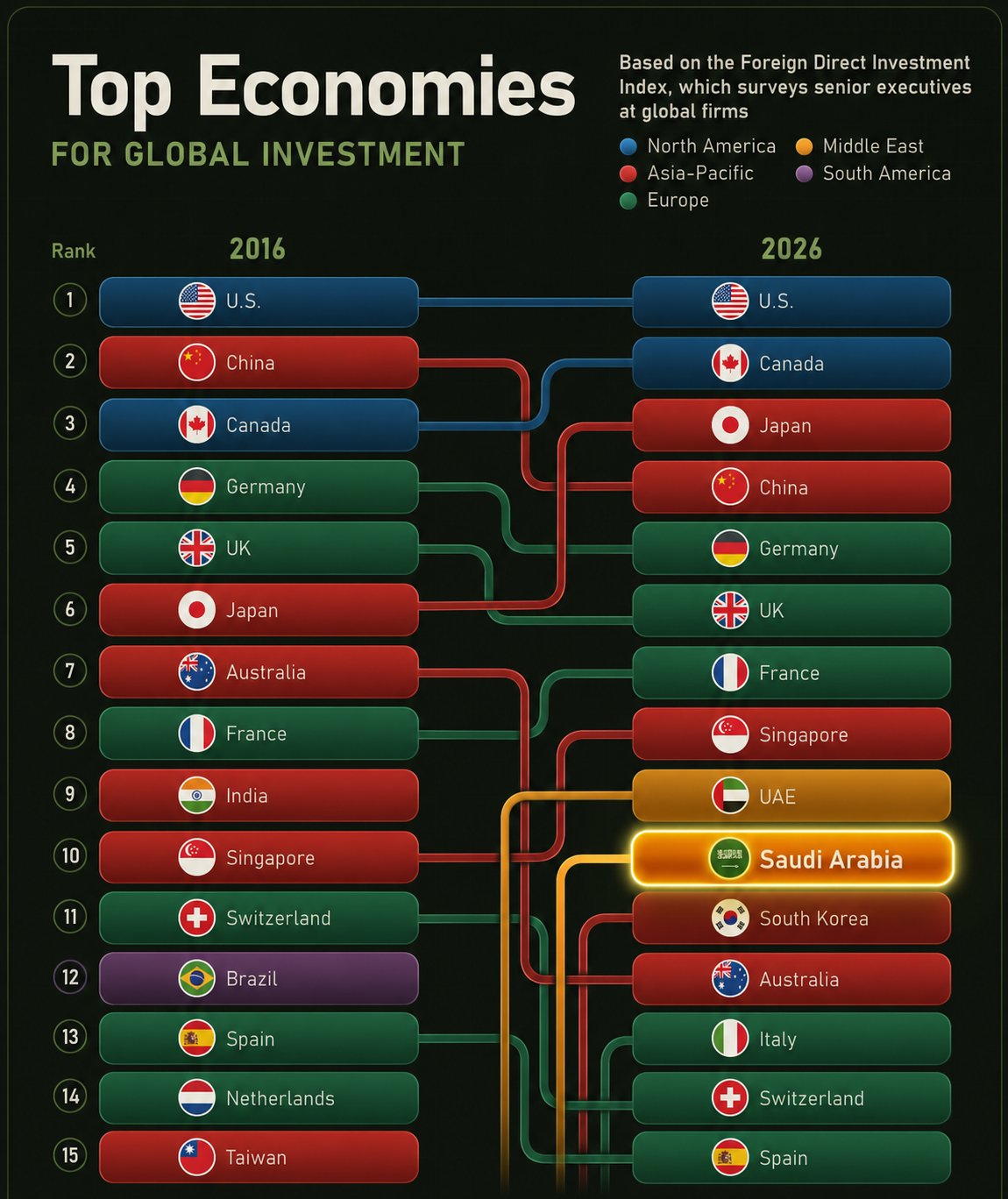

Saudi Arabia ranks #10 on the 2026 Kearney FDI Confidence Index — its first appearance in the global top 10, ahead of South Korea, Australia, Switzerland, and Spain. The kingdom climbed from 24th in 2023 to 13th in 2025 to 10th in 2026, with Kearney singling out Saudi Arabia alongside Singapore as the year’s standout "middle powers." Investors cite economic performance (33%), tech innovation (27%), and ease of doing business (27%).

Kearney’s annual Foreign Direct Investment Confidence Index — a survey of senior executives at global firms about where they intend to invest in the next three years — placed Saudi Arabia at number 10 worldwide in its 2026 edition. It is the first time the kingdom has appeared in the global top 10. Three years earlier, in 2023, Saudi Arabia entered the main Index for the first time at 24th.

The 2026 list reads: United States, Canada, Japan, China, Germany, United Kingdom, France, Singapore, UAE, Saudi Arabia, South Korea, Australia, Italy, Switzerland, Spain. Five places that conventional ranking exercises rarely move in three years.

The three-year climb

Saudi Arabia’s ascent on the index has been steady. 2023: first appearance at 24th. 2025: 13th. 2026: 10th. Kearney’s commentary attributes the trajectory to Vision 2030’s sustained delivery — what the report calls “remarkable momentum” — and singles out Saudi Arabia alongside Singapore as the year’s standout middle powers, the report’s own phrase for economies of growing geopolitical and economic relevance.

The middle-power framing matters. It signals that global investors are not just noticing Saudi Arabia as a frontier story — they are placing it in the same conversation as Singapore, a benchmark for institutional and regulatory quality. The peer set in the 2026 top 10 (the US, Japan, Germany, the UK, France, the UAE) reinforces that.

What investors are saying

Underneath the headline rank are the components that drive it. Kearney asks executives to weight markets on multiple dimensions; Saudi Arabia’s 2026 profile is unusually balanced for an emerging-markets entrant:

- Economic performance: 33% — Saudi Arabia outscores Germany (29%), the UK (31%), France (32%), and Australia (29%) on this dimension.

- Tech innovation: 27% — investors are reading the kingdom as a credible technology destination, not just an energy or capital one.

- Ease of doing business: 27% — a decade of regulatory reform under Vision 2030 (the QFI framework, the foreign-ownership law, the Regional Headquarters program, the property registry) is registering on global investor radar.

- Net optimism: 37% — among the highest globally for the three-year economic outlook.

The hard numbers behind the survey

Investor surveys are sentiment indicators; the receipts are in the actual capital flows. Net FDIFDI — Foreign Direct InvestmentInvestment by foreign individuals or firms that takes the form of direct ownership of a business or asset (10%+ stake), as opposed to portfolio investment (passive equity holdings). The kingdom's FDI inflows rose from SAR 28B in 2017 to SAR 133B in 2025.→ Read more in the glossary inflows reached SAR 24.9 billion (~$6.6 billion) in Q3 2025, a 34.5% increase year-on-year. Full-year 2025 inflows were SAR 133 billion — roughly five times the 2017 figure.

The cumulative stock tells the same story. Saudi Arabia’s total inward FDI position stood at roughly SAR 1.1 trillion in 2025 — a doubling since 2017. That cumulative depth is what global executives are pricing into their forward-looking confidence scores.

The emerging markets context

On Kearney’s separate Emerging Markets Index, Saudi Arabia ranks third for the third consecutive year, behind only China and the UAE. The persistence across consecutive editions distinguishes Saudi Arabia from one-off mover countries — investor confidence has held through three full survey cycles, not just spiked on a single event.

The PIF dimension underpins this. The Public Investment FundPIF — Public Investment FundSaudi Arabia's sovereign wealth fund. Originally established in 1971 to hold state stakes in domestic industrial champions like SABIC, it was designated under Vision 2030 as the primary instrument for economic diversification. Assets grew from SAR 720B in 2017 to SAR 3.41T in 2025.→ Read more in the glossary ranks roughly fourth globally among sovereign wealth funds by assets under management, and its anchor-investorPIF — Public Investment FundSaudi Arabia's sovereign wealth fund. Originally established in 1971 to hold state stakes in domestic industrial champions like SABIC, it was designated under Vision 2030 as the primary instrument for economic diversification. Assets grew from SAR 720B in 2017 to SAR 3.41T in 2025.→ Read more in the glossary model has given Tadawul listings, gigaproject debt issuance, and joint-venture announcements a depth profile that thinner emerging-markets venues typically lack.

For the first time, Saudi Arabia sits inside the global top 10 for foreign direct investment confidence — ahead of Switzerland, Spain, Australia, and South Korea. Three years ago, it wasn’t in the top 20.

What the report itself flags

The Kearney commentary is not unqualified. It explicitly notes that regional conflict in the Middle East may weigh on short-term FDI prospects. The kingdom is, however, described as comparatively less exposed than some regional peers, given its ability to divert oil exports via alternative pipelines and its continued public-sector-led investment supporting domestic activity. Strong economic fundamentals and infrastructure assets are described as protective against longer-term capital flight.

The report also notes that Saudi Arabia has incorporated health-sector transformation into its broader Vision 2030 goals — a signal, in Kearney’s framing, that the kingdom’s industrial policy is extending well beyond energy into human capital and diversified sectors.

What it means for citizens

External investor confidence isn’t an end in itself; its citizen-side consequences are concrete. More FDI translates into more in-kingdom employment options for Saudis: foreign firms hiring locally, multinational regional headquarters under the RHQ program, joint ventures requiring Saudi engineering and management talent, and a deeper services economy around the inward capital. The earlier “Vision 2030Vision 2030The kingdom's overarching economic and social transformation program, announced in April 2016. Built around three themes: a vibrant society, a thriving economy, an ambitious nation. Sets quantitative targets across labor, tourism, housing, healthcare, and other sectors, all benchmarked to 2030.→ Read more in the glossary” arc — Saudization, Nitaqat, and the localization decade — built the supply side of the labor market; the FDI confidence trajectory is building the demand side that absorbs it.

Metrics referenced

Continue reading

The localization decade

Read separately, IKTVA, Nitaqat, GAMI, and Made-in-Saudi are four different Saudization tools. Read together, they’re a stacked, decade-long attempt to localize a national value chain — an industrial-policy experiment whose cumulative effect has moved the headline numbers further than any peer effort in the same window.

70%· 70% of Aramco's supply chain — Made in Saudi

The Tadawul decade

Between 2015 and 2026, the Saudi Exchange went from a closed national bourse with marginal international weight to the largest emerging-markets equity destination outside the BRIC economies. MSCI EM inclusion, the Aramco IPO, the post-Aramco listing wave, and the PIF anchor-investor model rebuilt Saudi capital markets in a decade.

SAR 133B· Global capital coming to Saudi